[Update] Dish Network (NAS: Dish) - Top Three Questions

[Update] Dish Network (NAS: Dish) - Top Three Questions

My take on JPM's Top Three Questions for Dish

Given the recent JPM reports that make a clear bear case for Dish, I thought I’d share my thoughts on a few of their points. The great thing about this JPM report is that although they model in the 5G enterprise/IoT opportunity as a free option, they’re suggesting an equity value equivalent to current prices. If that’s the case, in my opinion, Dish should be a strong buy instead. JPM explicitly states they don’t understand the enterprise opportunity, and with that, they don’t value how the AWS developer ecosystem improves speed to market or how Dish plays a key role in the enablement of their edge services. To pair with the upside opportunity, unlike JPM, I think there are clear catalysts in the NTM like MWC at the end of the month with AWS, their Vegas launch, retail mobile numbers in Q4/Q1, and the possibility that the street understands the true value behind Dish/AWS.

1) Cost Advantage

While wireless is a scale game, it doesn’t make sense to compare legacy encumbered spectrum with Dish’s spectrum that’ll be exclusively be used for 5G since legacy caters to 3G, 4G, and 5G and shouldn’t just be amortized by 5G costs. As a result, cost/GB math isn’t solely dependent on which carriers have the most spectrum, and at the same time, Dish’s O-RAN architecture allows them to reduces capital spending from a variety of angles:

AWS partnership: Industry experts that I’ve chatted with privately have suggested that this partnership should reduce costs in the range of billions. They don’t need to pay for the upfront server costs like Rakuten and while they’ll get hit with OPEX as they scale, AWS’s developer community may be a higher ROI for Dish.

Tower Providers: Most of the towers based on building permits in Vegas are co-locations which also mean that fiber is already laid for those locations. Fiber and tower players are likely biting a significant upfront investment because of its strategic benefits in the long term. For towers/fiber, there are incredibly low incremental costs to adding new customers, and in exchange, they get a strong stream of recurring revenue. It makes a lot of strategic sense for these players to help Dish in short term because of the dividends another national player pays them in the long term.

Lease Costs: Dish takes up less space on each tower because of virtualization, so as a result of this, they pay less since tower providers charge based on sqft used.

Maintenance: With virtualization from day 1, maintenance capital expenditures should be significantly lower, and Dish doesn’t need to maintain soon-to-be legacy technology like 4G. This is a cost advantage unique to Dish. While legacy operators are switching to O-RAN, they are still building on top of legacy equipment so they aren’t able to enable the “zero trust” security model that Dish is able to do via greenfield.

With this, the 10B sounds more reasonable, but in the NTM, with the deployment of Vegas, there will be more granular detail that exposes the real costs versus hypothetical. With sell-side models already pricing in 15B+ for capex, more information will likely help Dish more than it hurts. Additionally, Dish will likely launch their retail wireless division at the end of the year, and with that, there will be clarity on their pricing for consumers, and what that implies for their cost/gb to service. This game is also not zero-sum, and if all providers switch to O-RAN and gain these benefits then that’s great too. Lastly, Ergen stands to gain little by suggesting the 10B capex requirement. Everyone in the industry questions that number, current analysts price in higher capex, and it paints Mr. Ergen as untrustworthy. With this, it’s important to reflect and rationally understand why that number MAY make sense. Charlie, with a significant amount of his net worth tied into Dish, likely isn’t spitballing random numbers when his incentives are tied directly to the business.

2) Spectrum Issues

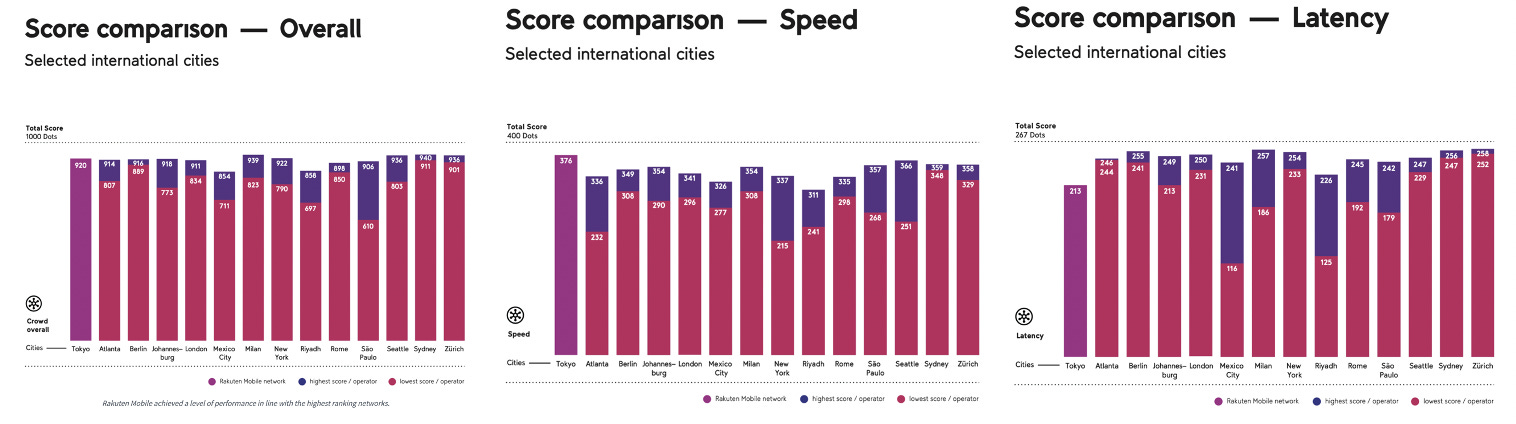

Network quality is no longer just dependent on speeds/coverage, but it’s also dependent on security, ability to control the network, and ease to set up with APIs especially on the enterprise side. These are aspects where Dish arguably has a competitive advantage. Nonetheless, JPM suggests that these legacy providers are spending 5-10x what Dish is spending so Dish has no chance of competing on network quality, however, they forget that these legacy providers are spending money to virtualize large parts of their network, maintaining 3G/4G, and then also building a non-cloud native 5G first before going O-RAN. Given this, it would make sense why the capital spends differ, but nonetheless, they argue that network quality would be worse given Dish’s lack of spectrum paired with lower capital spend. If we look at Rakuten’s latest report two days ago, the speeds look great although latency is on the weaker side driven by their lower band spectrum.

3) Enterprise / IOT

JPM admits they are not “knowledgeable enough to have an opinion” for the enterprise / IoT market yet publish a model on Dish, whose future business is clearly focusing on the enterprise. While valuing it as a free option, their estimates miss out on the significant optionality that 5G provides Dish on the high-margin services side and unlimited use cases that AWS’ developer ecosystem enables.

Dish may lack experience in enterprise compared to their peers, however, that would then discount the Amazon and Dish partnership. Amazon on the other hand is one of the most experienced at enterprise sales, and their incentives are aligned with Dish given the monetization opportunity they have with enterprises’ data that will be processed on the edge. Enterprises may choose AWS services, and then get connectivity from Dish in order to enable their IoT plans for example.

Although 5G will be ~10x more expensive than WiFi solutions, both products are not apples-to-apples, the point of 5G is that it offers new functionalities, and as a result, the ROI math changes. Currently, IoT adoption is low because of how complex enterprise networks are today with the need for WAN, multiple LANs, ISPs for indoor connection, wireless providers for outdoors, MPLS/VPN, and then Wifi/Bluetooth, etc... A network with that much complexity means it’s harder to manage data, automate processes, and run a network without a network engineering team. Similar to days prior to Twilio where enterprises needed 10+ engineers to enable communication functions, the network prior to 5G/Dish requires upfront costs and enterprises would need LAN Engineers to maintain the network. With end-to-end automation built into the network for maintenance and APIs that simplify network setup and application delivery, enterprises likely no longer need that sizeable team resulting in lower costs and higher adoption. With 5G, slicing, and SD-WAN, enterprises are able to simplify their processes into buying specific slices that meet their needs, and then can process low-latency data applications at private mobile edge computes. Customers are buying AWS functions for the IoT services / APIs, but now need a 5G service to enable that functionality. That’s where Dish steps in, and although this may seem like Dish is in the back seat, Dish will likely maintain margins on the connectivity side since Amazon sees a bigger opportunity on the data. Amazon wants to commoditize data access and Dish is an early and willing partner to use their network to enable AWS cloud capabilities.

While 5G use cases are in their nascency, Amazon makes it easier for developers to create potential applications with existing services like AWS IoT Management or analytics features like Amazon IoT SiteWise that reduce complexity for deployment, and 5G as a whole simplifies the process of having an enterprise-wide network. These lower barriers should spur adoption especially since speculated 5G use cases are high ROI — ranging from improved security, secure network access for employee phones (e.g. Walmart), or low latency applications that enable cost-cutting. Who knows what these applications will be, but it’s intellectually dishonest to not consider the significant optionality that 5G offers.

While there’s significant execution risk since Altiostar/Mavenir are new players in a world of experienced Ericcson/Nokias, current prices already reflect a significant amount of that priced in uncertainty.

Now, I think there’s a huge misunderstanding of management quality at Dish. So much so that JPM places an arbitrary 20% discount on valuation due to Ergen’s control of the company. While Charlie has "hoarded spectrum” for the last decade, I think the spot they’re in now likely creates more value for Dish shareholders than if they built it say 2-3 years ago. Their patience removed a lot of technical risk with O-RAN and this architecture is arguably the only reason they’ll be competitive in the wireless space. Charlie has also been able to maneuver around different requirements and end up in a decent spot that’s riding a pretty powerful secular wave. There are arguments like for example, Dish could’ve been a better Roku competitor with Sling or they should’ve shifted more capital to streaming, but at the end of the day, their satellite TV business, despite its secular decline, is in a much better spot than DirecTV. While Charlie doesn’t have the best reputation on Wall Street, it’s important to remember that his net worth is tied in this business and to think about where Dish could’ve been if he didn’t load up on the spectrum auctions. Regardless, he still needs to show the street proof that they can execute on this thing, but the AWS partnership is a sign in the right direction.

Thanks, and again please send feedback to my DM (@HCompounders). Thanks!