Tucows (NAS: TCX) - A bet on CEO, Elliot Noss, and the company's DNA

Hi readers,

The name of this newsletter was inspired by Mohnish Pabrai, and his coined term, “Hidden Compounders”. These companies are what he classifies as the next Visa like investments that just happen to be uncovered. Learn more about his thought process here. The companies I’ll feature won’t necessarily be as cheap as Pabrai traditionally likes, but they will all have the same qualities — hidden moats, long growth runways, and terrific operators.

Each month or so, I’ll publish a qualitative assessment of a business that I think fits these characteristics. Please don’t take anything that I publish as investment advice. My main goal is to shed some light on what makes these companies great rather than what makes these companies great investments. This newsletter is also a way for me to document my research publicly, so I can learn more through the discussions that are created around the companies that I write-up. Please follow @HCompounders on Twitter if you want to engage in such dialogue.

Lastly, I’d like to thank everyone — from industry professionals to my classmates — who helped me with this first piece. Although many of them would like to stay anonymous, I’m extremely grateful that this community was willing to extend their time to help out a novice writer.

Book Recommendations

Before every pitch, I’ll include the books that inspired each of these write-ups.

The first is Professor Heskett’s The Culture Cycle: How to Shape the Unseen Force that Transforms Performance which was suggested by Paul Black of WCM on an older episode of the podcast, Capital Allocators. The second and more obvious recommendation is Fiber: The Coming Tech Revolution―and Why America Might Miss It written by Harvard Law Professor, Susan Crawford. This is a must-read if you’re interested in understanding a major cause of the growing urban / rural divide that we are seeing in the US today and the amazing movement that is trying to fix it.

Overview

The more I’ve studied Tucows, the more I notice that the company is simply a billing and customer service business. They may run three separate businesses — domain registry, pre-paid mobile services, and fiber internet — but the one thing they all have in common is offering a world-class customer experience that they leverage to win in what are traditionally considered commoditized businesses.

With Tucows, shareholders get two low growth but cash generative businesses that fund a ~20% IRR investment. All-cash generated is highly predictable, recurring, and acyclical. This money is deployed into a highly demanded market that produces natural monopolies, has less than 90% penetration, and has low maintenance costs / capex (60% long term net margins). Tucows just has to bite the large upfront investment. Sounds like a perfect pair — a previously low growth, capital-light, and cash generative business can now fund their newest business which generates high returns but requires significant upfront capital.

Tucows reminds me just a little bit of AMT or Buffett and Railroads, and we all know how those returns turned out. If this doesn’t excite you, I don’t know what does!

Tucows’ Competitive Advantage - Culture

Tucows’ culture is essential to understanding how any of their businesses function. I became inspired to look for companies that had a great culture after reading The Culture Cycle: How to Shape the Unseen Force that Transforms Performance, where Professor James Heskett runs through culture as a competitive advantage.

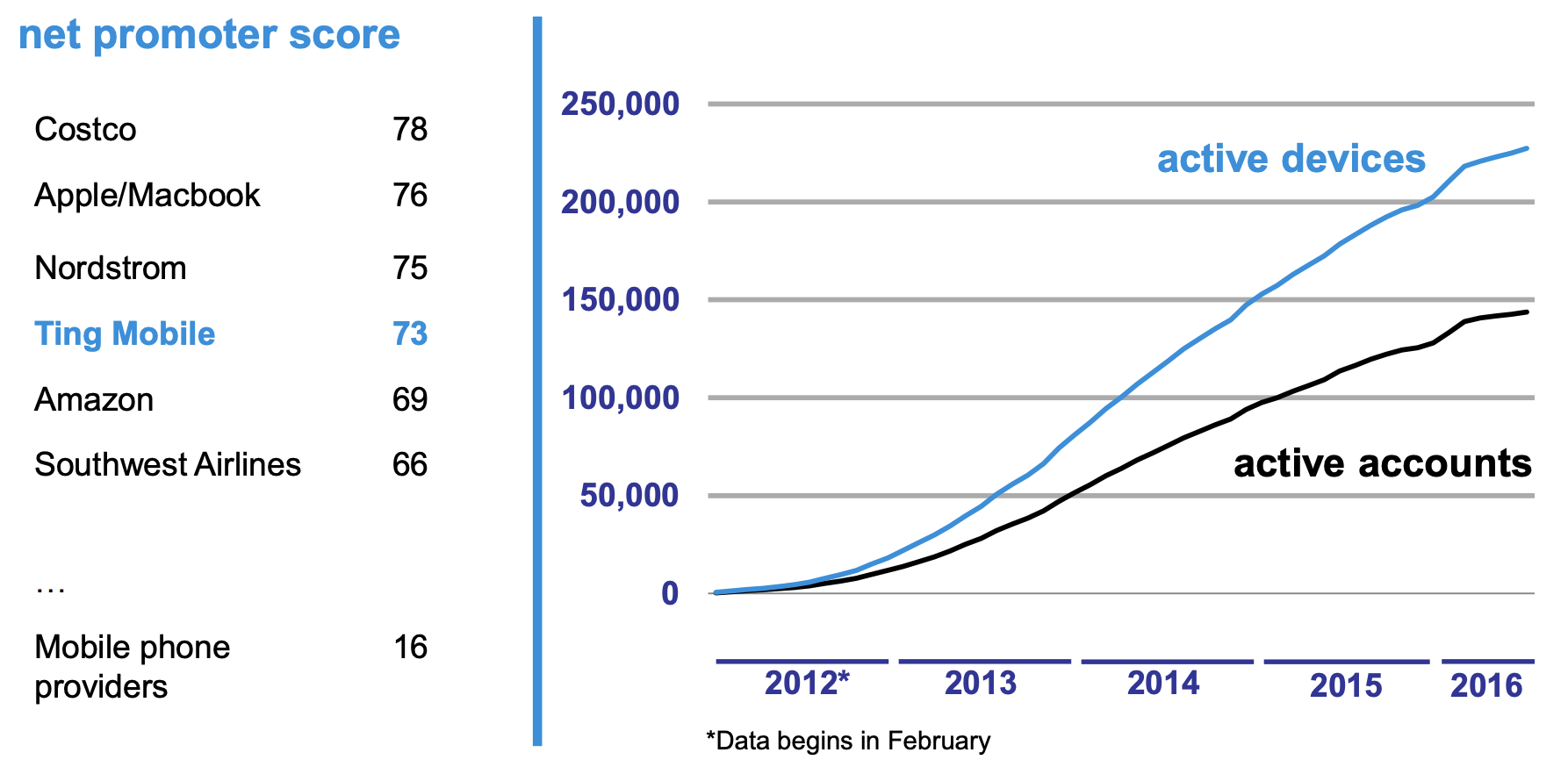

When I noticed that 11% of customers for Ting Mobile were referred by existing customers, I immediately thought of Heskett’s Four R’s (Referrals, Retention, Returns to Labor, and Relationships), or signs that a company had a great culture.

As a result, I went looking for the source.

From the company’s mission,

“All of our companies…are built on the premise of delivering superior value and industry-defining customer experience,

to the CEO regularly checking the Charlottesville subreddit to understand what his customers want, one thing was clear — Tucows obsesses over their consumers.

This Reddit thread indicates that this obsession is reinforced through employee incentives

You're only "graded" on one thing -- customer satisfaction. There are no call times / wrap-up time metric. No sales. No one whose job it is to mark X number of calls each month and give you an internal score (which I know creates anxiety at other jobs, especially if hours / pay / bonuses are based on this). A call could last 2 minutes or 2 hours -- and at the end, you email the customer a summary. Once the issue is fixed, you "solve" the ticket which generates a survey the customer can (optionally) fill out. That's it. That's the metric that matters. My manager has never said "hey you're on a 90 minute call -- wrap it up!" because he knows the woes. Sometimes you're trying to fix Ethernet drivers or you're dealing with a beginner.

Just like the Toyota production line was a function of constant small improvements that were suggested by their employees, Tucows’ customer service evolved as employees discussed improvements with their open management teams.

“We have 1 on 1 meetings with our managers every week…usually I say to my manager "we currently do things this way. it would be more efficient if we added a button to do XYZ. saves a few clicks and I'm not sitting there re-doing these steps over and over" and he goes "lemme write that one down. I'll speak to Product Management and see if our tools allow us to make that change."

For another company to replicate their culture, they would need to completely revert everyone’s incentives and roles. Noss has cultivated this over two decades, so I doubt one of their peers will be able to immediately replicate the process at scale.

Whether it’s their domain business, Ting Mobile, or the internet, it’ll become clear how their culture translates into creating differentiation, through customer service, in these hyper-competitive businesses.

The Initial Journey - Domains and Mobile

Tucows (NAS: TCX) started in the domain business in 1993. Since then, they’ve grown to be the third-largest domain registrar in the world behind companies like GoDaddy.

Their domain registry business can be broken down into three things:

1) With their products like Hover, they have around 11 Million names under their control which they’ll milk cash from as customers continue to register, renew, resell, and transfer these domains.

2) Tucows provides value-added services/management to resellers (OpenSRS, Ascio, EPOG, and Enom) of their domains like Shopify or Squarespace like security or email so that these companies can focus on their core business. There are tons of services out there like this, but the Tucows’ customer service continues to act as a competitive advantage in this space.

3) They also have services like Platypus which cater specifically to Internet Service Providers (ISPs) that integrate with their domain services like OpenSRS.

Through his experience with Platypus, Noss knew exactly what he was getting into with Ting. To quote Noss, “We have always had a deep belief based upon a couple of decades of experience that the ISP business produced incredible net margins at scale and that it could be done better than it was being done.”

After realizing the limited incremental TAM in the domain registry business, Noss redeployed his capital into the MVNO space through Ting Mobile. An MVNO is a service that provides a wireless connection on top of an existing network. Ting used Sprint’s existing network to offer pre-paid phones. It’s generally hard to create unique value as a small or emerging MVNOs which caused Dinsey, Best Buy, and others to struggle, but Ting has still found a way to deliver value to their customers. Their success in the space can be characterized by a few things

Driven by excellent customer service, Tucows has been able to get around a 2% churn while the industry average in the MVNO space is closer to 4%. The lower churn was a result of Tucows’ top-notch customer service which many customers weren’t used to in the MVNO market. Tucows then passed on the savings through the low churn to their consumers through pay-for-what-you-use plans which led to even happier customers. This has led to skyrocketing NPS resulting in 11% of their customers are also through Referrals.

As of Monday, Tucows announced a partnership with Dish where Dish acquires their customers and Tucows becomes their MSE, or Mobile Service Enabler. Although the details are limited, Tucows must’ve realized that Dish has a structurally low-cost advantage given their new partnership with T-Mobile which they didn’t want to compete with. Anyways, Tucows will now get to focus on their core competencies, billing, and provisioning, as an MSE

Capital Allocation / Management

No matter which Elliot Noss Interview you listen to, his love for each line of their business shines through. His long term focus and track record as an allocator is top-notch, and he owns a little less than 10% of the business (not sure if this qualifies as owner-operator territory). This, combined with his obsession around the customer, 20 years of experience as a CEO, and love for both Munger and Buffett have enabled him to return ~20% for his shareholders for the last 20 years.

Through 8+ Dutch Auctions, Tucows has repurchased over 50% of its shares. Noss views buybacks as one of the tools in his toolbox, but he mentions that “it’s a balance and the choice between how much money we put in the ground in fiber, how much money we spend on the stock, [and] how much money we look at other opportunities.” Noss’s awareness about all of his potential investments forces him to be opportunistic about his buybacks. He most recently repurchased some shares at ~$50 (soon after the Kerrisdale short was released), but in the past, he’s been angry about not having enough in the buyback program because he wanted to take advantage of the value that the market was missing (e.g. when it traded at $20 in 2016). Recently, he’s been cautious about acquisitions in the ISP space because he doesn’t want to overpay and is careful about buying businesses with a culture that integrates easily (e.g. Cedar Networks). To be frank, all of this has left me admiring Noss as an operator, allocator, and innovator.

Ting Internet - The third cash cow

Ting Internet was born in 2015 when they acquired a small Fiber focused ISP in Charlottesville, VA. Fiber is kind of like a SaaS business — a large upfront investment that has recurring streams of subscribers after. It’s a scrappy, little business that takes advantage of the current incumbent ISP’s complacency without waking them up from their hibernation of underinvestment.

Fiber might be a relatively new space for a lot of my readers, so Professor Crawford’s book, Fiber: The Coming Tech Revolution―and Why America Might Miss It, and her related interviews are going to act as the basis for most of the introduction on Fiber.

Fiber isn’t a new technology, but it’s long been underappreciated in the US. It has a few key benefits over the primary incumbent, copper wire / DSL:

1) Since Fiber is made of glass strands, it uses light rather than electric pulses to transfer data at faster rates. Using light, fiber optics are able to transmit information for miles without interruption, unlike copper which is susceptible to nearby electrical interferences. Many folks in rural areas have lagged internet access to the point at which they can’t even load a video, but fiber would solve all of that.

2) There are also almost no maintenance costs for fiber since “connectors are effectively sealed from dirt in patch panels, and splices are sealed in enclosures that prevent moisture from entering. There is no need to disconnect terminations to clean, inspect, or test them.”

3) Lastly, Fiber lasts as long as copper with a functional utility of somewhere between 20-40 years. However, Fiber “is essentially future proof…to improve that capacity, as the science of photonics improves, you can merely swap out the electronics producing the photons—the glass stays in the ground or on the poles” making it unlikely to be replaced by disruptors.

Other countries like South Korea and Sweden have completely moved to Fiber because of its known benefits. More importantly, over 500 US rural towns are starting to adopt Fiber because they recognize the competitive disadvantage that copper wire / DSL puts them at for education and economic development. Union Square Venture points out that “a modern communications infrastructure is the most important investment any community can make to expedite the transition from a 20th century economy based on undifferentiated manufacturing to a 21st century economy based on highly specialized manufacturing and services.”

Long haul Fiber in the US is quite common since telecom companies need fiber to run through cities in order to enable 5G. America lacks FTTH which is Fiber to the Home, or last-mile fiber connection. Only around 10% of Americans have access to FTTH. This is driven by the investment in fiber not being in a cable company’s best interest to improve this situation (especially in rural areas). The incumbent’s logic is pretty clear. Why improve, when I already have pricing power / monopoly in these areas.

Like electricity, most initial fiber deployment is in urban areas, to minimize investment downside. Even in the 1930s, only 90% of farmers had access to electricity, and a similar trend is emerging for Fiber. If more money flows into Fiber because of an equivalent bill to the Rural Electrification Act (REA), it’ll encourage others to build the fiber infrastructure and allow Ting to execute what it’s best at — customer service. This likely won’t happen though given that the FCC is already funding programs just to get rural areas to 10 mbps+.

Barriers for larger players

1) Patient Capital

There is so much demand for fiber and the investment opportunity looks somewhat attractive, so why aren’t more players moving in?

Since Tucows and Google / Verizon have different company profiles, Tucows is arguably under less public scrutiny to focus on the more flashy, immediate return, and capital-light projects. Google had to exit because its shareholder said Fiber was too capital intensive. Verizon would’ve been pressured to put more emphasis on mobile 5G or AT&T with entertainment if they dedicated too much time to fiber. Even Crown Castle has recently gotten pressure from Elliot due to the capital intensity of Fiber. Crown argued that initial cash yields of Fiber were 7% which were greater than the initial 3% yield for Towers (h/t Masa Capital on Twitter). Naysayers were also down on Towers, but now if you ask anyone, they’ll say it’s a no brainer:

Read this fascinating piece if you’re curious about why bigger players likely won’t be entering this space anytime soon and why they haven’t before. And this too if you’re looking for more.

Tucows’ shareholder base is quite small and most of them understand the long term nature of the business:

It has always been the case that our shareholders have appreciated our focus on long-term cash flows, not GAAP accounting and quarterly profits. They have appreciated our willingness to be bold when pursuing long-term opportunities.

Additionally, Tucows has two other cash creating businesses, so they are able to internally fund these returns without having to rely on outside capital. Two other players — Boston Omaha and Allo / NelNet — are able to execute with the same structure. Smaller companies need debt, so financing then acts as a barrier since the payoff period is on the longer side. They also lack the collateral necessary in order to take on the debt. This piece details why small companies have struggled to enter, and it’s simply a matter of funding. Some one-city players have entered the space, but it’s almost impossible to scale due to the payback periods on these projects. Tucows’ negative working capital, or quasi-float, is also a helpful funding tool for the firm.

2) Economics

Noss claims that the IRR for fiber deployment is a function of four things: take rate (reminder, this is the rate of adoption in a city), long term net margin, cost of the build, and the terminal value.

Larger players for obvious reasons focus on larger markets first for fiber deployment. However, this creates a lot of difficulties. Whether it’s 1-2 small fiber players, cable providers, their non-fiber services, or even DSL, each service slowly scrapes away at the potential take rate since it’s hard to convert customers from “ok” services, primarily cable, even if Fiber is a better product. As noted in the Boston Omaha annual letter, permitting costs in larger cities are quite expensive which continues to push down the IRR, however, in smaller areas the towns are more incentivized to work with the companies to get those permitting costs down. Google also failed because their grand entrances into cities oftentimes triggered a competitive response by the incumbent who started building out their own network. For these reasons, the IRRs are going to be lower for these larger players causing industry leaders like Cogent to be vocal about fiber’s terrible economics.

The reason why bigger players won’t bother with Ting Internet’s game is twofold.

i) Fiber is localized as there is a lot of grassroots involvement in order to get adoption.

ii) The areas that Tucows operates in are incredibly tiny, on average less than 20K addresses. Therefore, it makes no sense for a company like Verizon Fios to invest a significant amount of time and energy into something that won’t make a dent in its top line. Ting towns are so tiny and their current ISPs provide 2nd or 3rd rate services like DSL or cable, with terrible customer service, which helps them achieve higher take rates than their large peers. Their localized approach and world-class customer service help convert customers away from the “ok” services. Tucows has no location-based strategy since they go wherever they realize take rates will be high since they know that’s the key driver of this game.

Companies will only see value in the deployment of fiber if they have both the patience and the availability of internal capital. Bigger players don’t have the former, and smaller players lack the latter. As a result, there’s only a small intersection of companies that decided to play in this space.

Why will Tucows generate better economics than their peers?

One thing that I need to get cleared — other players are going to succeed too and Tucows simply can’t capture every city. However, when they compete with others, Tucows will win almost every time.

The Benton Institute for Broadband and Society says there are five models in which fiber can be deployed: Full municipal broadband, Publicly owned, privately serviced, Hybrid ownership, Private developer open access, and Full private broadband.

The full private ownership model could squeeze out Tucows, but here are a few reasons why that won’t happen. First, Tier 4 cities (<1k households) are often the main ones that rely on this model since “there may not be any options for private cooperation” in those cities given their economics. Many folks definitely prefer private-led fiber deployment since public only models are incredibly capital intensive and have longer payback periods since they lack expertise in the space. As a result, my hypothesis here is that many of these towns build out municipal fiber not because it’s their first choice but because it’s their only choice like in Coon Rapids, IA.

When it comes down to the other four models, Ting is able to use leverage its culture into winning over customers.

1) Great customer service

If you take >5 minutes to browse their subreddit, you’ll get a clear understanding of the level of customer service that I’m talking about. A reminder that this is simply a function of their culture that is centered around obsessing over the customer. Tucows leverages this into fantastic customer service to convert customers from DSL/Cable, and to beat out any company that challenges them in the public/private fiber model.

This example comparing both GigabitNow and Ting Internet acts as evidence that Ting has a super customer service advantage. In this example, a customer has to wait 15 minutes to get on the phone with a GigabitNow rep before getting kicked off the line. This customer is able to get a hold of a Tucows’ employee in both methods in >5 minutes. Other smaller players like Ziply Fiber, who bought a piece of Frontier’s Northwest Fiber business are also known for terrible customer service. With Fiber, people not only want fast internet, but they also don’t want to deal with a company that doesn’t exhibit terrible customer service like Comcast — luckily Ting checks both off.

Tucows also created proprietary backend software for customer service for their other two businesses which act as a competitive advantage since they can customize it as they get suggestions from their employees.

2) Community-oriented view

It all starts with their focus on the consumer. Everyone, from Professor Crawford to Noss, believes that Fiber is a hyper-localized game, and their focus on the consumer helps them outscore their competitors. Tucows deserves credit for managing these hyper-localized operations at a national scale, but it’s simply a function of their culture pushing for an obsession around the customer which others haven’t been able to scale.

Spanish Fork, UT take rates are hitting around 78% overall compared to Ting’s 50% estimate, and near 100% take rates in some neighborhoods because of this community orientation. Although Spanish Fork’s fiber is run by the city, it acts as evidence of what the take rates can be when a company’s name and internet connection become synonymous with each other. With their best-in-class customer service and as a result, referrals, Tucows can potentially reach those levels too outstripping their competition.

3) Reputation

In the Benton Institute paper, Ting was used as 2 of the 5 cases that they discussed. That, combined with the fact that they say they meet with at least 2-3 cities a month when they take maybe 2-3 additional projects a year max gives me confidence that they have a great reputation and / or have a strong demand. They’ve also built quite a reputation with Ting Mobile which has a loyal of its own.

Tucows also builds a great name in the broader area that they use to get attention from nearby communities. For example, they used their glowing reputation in Holly Springs to gain traction in nearby communities like Wake Forest and Fuqua-Varina. This attention even before entering the town in combination with referrals means that Tucows doesn’t need to spend as much on SG&A when entering the town.

With this reputation, they likely get first priority on a lot of these projects. With this strong stream of opportunities, they’ll be able to choose cities where the other competitors are underserving the population or cities where there are Ting loyalists, something they measure through a voting platform. Examples like the one below indicate how their reputation helps out.

4) Natural Monopoly

Once Tucows enters a market, it makes zero sense for other fiber players to enter since they have to have a unique value prop over Tucows in order to steal Tucows’ customers. Take Rates are the single most important component for the IRR because there is so much variance in its value — easier to predict the cost of the build, margins, and terminal value. But if you have to make the same investment with a take rate half the size, you’re going to get returns below the cost of capital. There are likely no disruptors too since Fiber can easily be improved (remember that you can just replace the endpoints!). There are two conditions to this forming: it has to be fully private fiber model and the firm deploying fiber needs top-notch customer service

So…what do the economics look like?

For starters, everything below is quite rough. I’ll do a more detailed take on valuation in the coming weeks if there is interest.

The Benton Institute looked at over “1,000+ municipal broadband programs, analyzed publicly disclosed information and case studies, and conducted in-depth interviews with key city officials”. With this data, they predict a city will see a near 16% unlevered IRR if they were to deploy their own fiber using “average” unit economics. Since Ting has the scale, experience, and strong brand advantage, it’s not hard for me to believe that they’ll likely perform are better than “average”.

It’s easy to comp Tucows to other businesses, but this would be underselling Tucows’ management team who is able to create success in commoditized businesses as they did in MVNO space.

For this reason, my unit economics discussion is going to rely on Tucows’ disclosures which I have faith in for four reasons a) Noss’s track record b) they’ve become more transparent over time and haven’t stepped back from their original estimated IRR numbers even as they’ve seen their own data come in c) Noss’s understanding of the ISP unit economics due to their ISP billing platform, Platypus d) For the Sandpoint project, they mentioned that they’d move into surrounding neighborhoods if the core area was successful and they recently announced the expansion. It’s also important to mention that they are the only public company that discloses their fiber economics.

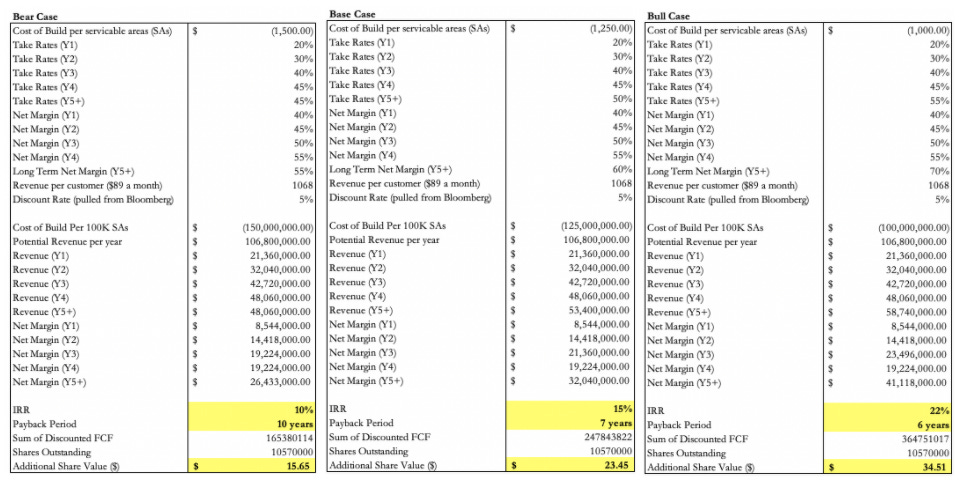

Using the assumptions, I get to some very attractive returns. First, I assume that all of the net margins converts to cash flow (conversion could likely be higher than 100% actually due to increased depreciation). Additionally, I do some guesswork on the short term net margins and take rates (Y1-Y4) which shouldn’t affect the IRR too much.

Management’s disclosures include a long term net-margin of above 60%, an upfront cost per serviceable address of 1000-1500, and take rates (20% by year 1 and 50% by Year 5). For the discount rate, I pulled it off Bloomberg, but it comes to around 5.4%. Lastly, for the lifetime of the fiber network, I use 40 years which is what Professor Crawford assumes.

The bull case goes a little above management expectations on take rates, but the 70% net margins and cost of build are both within range of their guidance especially since those are apt to get better as they understand where they can be more efficient operationally.

In the bull case, Tucows only needs around 200K Serviceable Addresses (SAs), or around .2% of all SAs (already at 45K and ramping) to get to their current ~$60 valuation. This would also be valuing their other two businesses at $0 which would be inaccurate. I understand that this is all very rough (ignoring a lot of discounting since these projects would be launched at different times), but you should start to get some sense of the margin of safety in this investment. Most importantly, they are able to deploy large amounts of capital at these IRR’s. They produced 40M in CFO last year which if fully deployed at a 20% IRR can produce around $10 in additional share value.

Most of their SAs will continue to come from public/private partnerships which require less capital intensity, but the IRRs for these projects will likely be lower (not enough disclosure to truly understand). Regardless, they’ll be able to deploy and recoup initial investment at much higher rates in this case.

Is this a 10 bagger? Maybe. On my back of the envelope math, they’ll have to get to 2M+ SAs which is still only around 1% of the market share. In order to get there, the capex would need to skyrocket, and the business would have to look fundamentally different. But, the reinvestment opportunities and competitive advantages exist to get there as over 90% of Americans still lack Fiber to the Home. There also isn’t much capital in the space due to the small overlap of companies that can compete in this space.

Evaluating this company based on its 5-6% revenue CAGR or its decreasing ROIC in recent years would result in an inaccurate characterization of the business. Since most of the returns on the fiber assets happen in the latter half of the fiber’s life, the ROIC is going to be decreasing until their fiber business becomes more mature. Since most of their recent cash flow is being deployed into fiber, you can’t expect too much revenue growth from their other businesses. With most of their revenue growth occurring in the later stage of the fiber deployment, there is going to be a lag in revenue growth so it’s not an accurate measure of the business.

Risks

Boston Omaha also mentioned that they will only go into markets with DSL / Copper since the take rates don’t work out if the competition is cable since the competitive advantage isn’t that high. Anyways, Tucows has continued to enter markets with cable yet feels confident in that 50% take rate. However, it is a key risk to note that Tucows may not hit that 50% because of some of the existing competition. Based on people’s current internet demands, cable is not noticeably worse than Fiber, but their differentiated customer service might be enough to get people to convert to Tucows. No matter who I talk to, one thing is clear — they hate dealing with Comcast or their respective cable provider. Also, if Tucows gets too large in a particular area, the largest regional ISP might take notice and try to put regulatory pressure against them. The key is not to wake up the giants.

Thanks to one of my close friends, I was notified that Musk’s Starlink and Amazon’s satellite internet services had gained traction. In the case this succeeds, it could severely decrease the reinvestment opportunities that Tucows has.

Hidden Moats Summary

Tucows’s growth lies in a market that has a small pool of capital but has more than enough reinvestment opportunities going forward. This all obviously depends on if Tucows has growing moats.

1) Shareholder base values Tucows’ focus on long term investments.

2) The niche markets that they serve don’t awaken the giants.

3) Their culture fosters customer services among other things that allow them to succeed in markets that others think aren’t possible.

4) Tucows’ reputation gives them an edge in regard to project sourcing and selection.

5) Their scale provides future operational efficiencies that’ll allow them to offer the lowest bid for many towns, not only helping them win contracts but also boosting their IRR.

6) The technology of fiber is future proof since you just need to change the glass boxes which protects them from new disruptors.

7) Fiber’s market is a natural monopoly creator since the economics don’t work out if take rates are divided among two players.

About me

For some background, I’m a rising college junior, and I’m just starting to get my hands around the beauty of investing. I have a lot to learn, so I’m always appreciative of feedback. Please DM me @HCompounders on twitter if you’d like to chat!

Hey I really enjoyed this post! You should do more write ups like this. Just subscribed!

Just a note about Tucows, I am researching it currently because of this post and finding it hard to justify the current valuation unless the IRR is low, like you mentioned a 5% discount rate/WACC in your article. Also finding it hard to predict future FCF because of the capital intensity of building out its fiber internet business. If you could do a deeper dive into that, that would be really cool. Also I would recommend trying to get this post on Value Investors Club.

Thanks a lot dude!