Dish Network (NAS: DISH) - Ergen's Pocket Aces

Building permits analysis indicates hidden opportunity on their enterprise business

Dish Network offers an asymmetric risk/reward with a 5-year IRR of 20%. In the NTM, based on my analysis of building permits in Clark County, there should be continued multiple expansion as their Las Vegas 5G deployment outperforms expectations. In the long term, the firm should likely beat priced in revenue and earnings estimates and see significant multiple expansion with long-term margins in excess of 20%. Dish’s use of O-RAN, a cloud-native architecture, is misunderstood as being disruptive only if it is able to deliver a lower cost/GB, but rather Dish’s differentiation from O-RAN will be driven by improvements in security or speed to market. Their capital-light deployment model, paired with high-margin enterprise services, in the range of 70% GM, could lead to new long-term economics for Dish. In this case, there should be a re-rate for the enterprise segment closer to a HSD/LDD cloud revenue multiple. Multiple expansion stories and concept stocks aren’t my favorite, however, with numerous deployment catalysts in the near term and reasonably priced in estimates, Dish’s story is more predictable than others. There’s reason to be skeptical as they are trying to build an entire network from scratch while failing to put anything together for the last decade; on top of this, they are creating new functions that have yet to be tested like functional APIs.

Execution

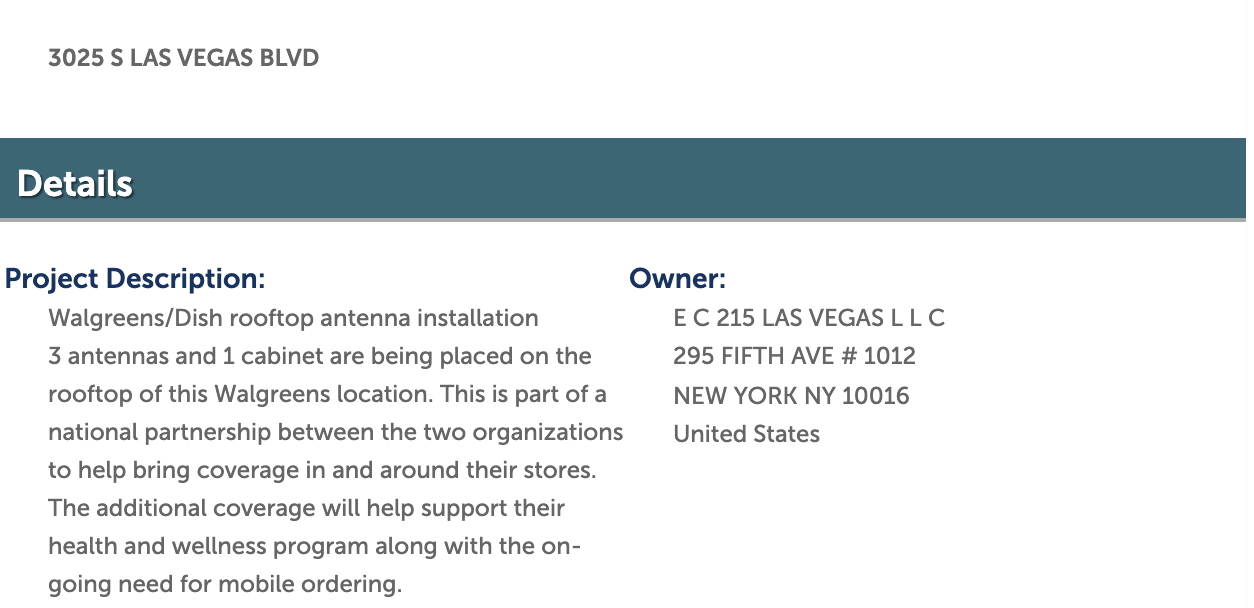

While their AWS partnership gave investors increased confidence in execution, Dish’s current price, despite recent price appreciation, still indicates uncertainty in the success of their buildout. From a Clark County database (link), there are details about Dish’s unannounced nationwide partnership with Walgreens.

The building permit (BD21-23238) for a Walgreens/Dish antenna installation states that “this is part of a national partnership between the two organizations to help bring coverage in and around their stores. The additional coverage will help support their health and wellness program along with the ongoing need for mobile ordering.” While this isn’t material for revenue / earnings estimates, this partnership has two main implications. First, Walgreens has already signed a 2-year contract with Verizon to offer fixed wireless to Walgreens/Duane Reed Stores. Given Verizon’s capabilities as the leader in enterprise 5G and their strong coverage, there’s likely no reason to sign with two providers unless they believe Dish offers differentiated value, likely, in the form of their flexible cloud-native network. Second, Walgreens is likely working with inside information on the execution of Dish’s build to feel comfortable about a nationwide partnership, in addition, to the fact that they think Dish will be on par with Verizon. Dish has other major enterprise 5G contracts locked in as well. These contracts were less explicit but were implied since either their 5G antenna descriptions were similar to the Walgreens agreement, were different than tower descriptions, or other wireless players didn’t have equipment at this address:

Hotels: MGM Grand (BD21-25656), Westgate Las Vegas Resort (BD21-26788), Westin (BD21-25595)

Smart Homes: The Estates at Highland Hills by Lennar (New smart home community featuring home automation like Ring DoorBell, Ring Alarm Security Kit, level lock, Mesh WiFi, and Liftmaster Smart Garage) - IMPORTANT NOTE: Dish stated their cloud-partner, unannounced at the time, would have a go-to-market strategy. Lennar could be one aspect of that given that Amazon and Lennar have been partners since 2018 to showcase Ring/Alexa. (BD21-23340)

Private Facilities: Draken International owned by Blackstone - Defense provider; they have the World’s Largest Private Tactical Air Fleet (BD21-27162)

Shopping Centers: Silverado Ranch (BD21-27877)

While there are potentially more in this dataset and in other counties’ databases, there’s now more proof that 5G offers significant optionality. Localized customers also mean that Dish will be able to monetize their network as they build it out; this should further reduce their capital needs from external sources. Dish has other opportunities like further expanding their partnership between its smart home installation branch, OnTech, and ADT, to enable secure 5G in homes and its Satellite TV / MVNO partnership with DraftKings to create play-by-play betting at homes and in stadiums.

Their recent partnership with AWS should also reduce capital needs since they are hosting much of the core and RAN on the AWS cloud and leveraging existing infrastructure with AWS unlike, their O-RAN peer, Rakuten, who decided to build their own CoTS servers. While Rakuten would gain more operating leverage as they scale, Dish likely realizes that the bigger benefit is AWS’s developer ecosystem. AWS enables faster speed to market on enterprise 5G use cases via CI/CD and allows Dish to use pre-existing AWS applications to scale its network. For example, Amazon’s EC2 Auto Scaling, allows Dish to dynamically scale its services that are hosted on the cloud. This allows Dish to better manage its operating expenses as they build out their network given that they’ll only pay for the number of customers that they have compared to hardware which requires an upfront investment. While the 10B deployment CAPEX amount that Dish is quoting seems like a low-ball, the same Clark County database provides job contract values for the installations. For some cell sites (8601 HELENA AVE & 3599 N LAS VEGAS BLVD) that host both Dish and other providers, the labor cost difference is 20K for the install and another 20K for electricity in favor of Dish. While labor for the installation itself isn’t the most important driver for capital expenditure savings, since Dish is able to cut labor costs by 66%, it likely means that the equipment installation reduction is significant as well.

On funding and capital needs, skeptics argue that AWS isn’t funding this network, but they’ve significantly invested indirectly (hint) into optimizing the cloud / edge for telecoms due to how strategic it is for them. Chairman, Charlie Ergen, implied that CSPs could be AWS’s next leg growth as he stated that Dish could be the biggest customer for AWS. Also, Amazon has greater plans like drone delivery, self-checkout Go Stores, warehouse optimization, smart homes (see Lennar example above), etc… which likely require a secure and cloud-native 5G. Amazon will be utilizing the service that they help build and the Lennar Smart Home example is a tiny step in that direction. More details will likely be disclosed later this month when AWS takes on the MWC with two Dish executives. Sign up here.

Also, a quick reminder that although Ergen has generated little shareholder value over the last decade, his interests are aligned with Dish given that he’s a 51% stakeholder in the business.

5G Market & Dish’s Differentiation

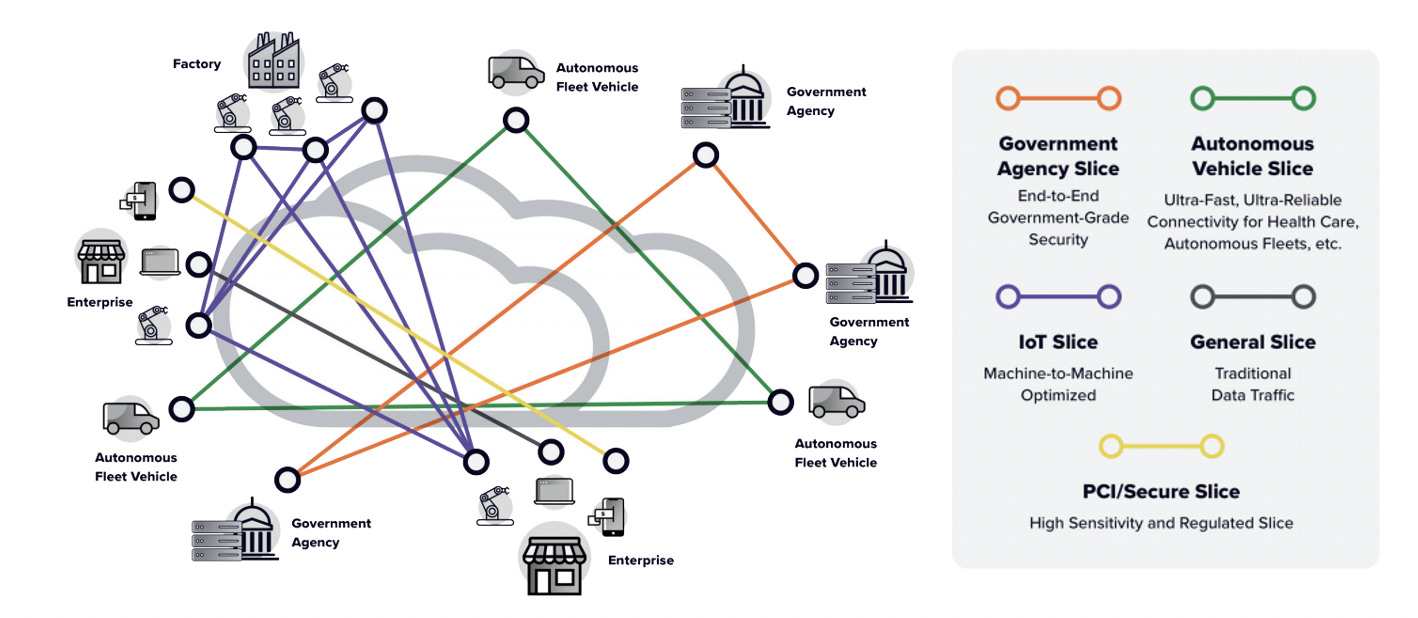

Apart from speeds, latency, and bandwidth, 5G’s architecture allows operators to slice the public network and create multiple quasi “private networks” within it. For example, there can be a slice dedicated for low latency gaming applications or one for higher bandwidth monitoring and tracking applications. Slicing improves 5G security as well as 1) CSPs can build in different security levels for each slice and 2) a breach in one slice would mean that other slices aren’t affected. Dish, and other providers, can sell access to specific slices as a part of “Network-as-a-Service” (NaaS) for a fraction of the cost compared to private networks.

While IoT and AVs are the classically thought of use cases for 5G, the TAM for enterprise 5G isn’t constrained to firms that want to build automated factories. Betacom recently raised money from industry leaders for CBRS enabled 5G networks that provide increased security compared to WiFi solutions. Their recent traction is an example of how a market opportunity exists for firms that may want NaaS for security, rather than speed/latency. For those who want to build IoT factories, security is an even more important factor since it requires thousands of devices, and as a result, thousands of more points of potential attack. With 5G, security improves due to slicing and added encryption, however, Dish’s O-RAN and greenfield network deployment is able to achieve security levels above their peers. For example, Dish’s partnership with Allot utilizes their cloud-native architecture to have real-time analysis of threats whereas legacy solutions preempt these attacks via a firewall. They are also able to employ a zero trust model where they audit all their suppliers to check the security parameters and embed an additional layer before deploying. This is something that legacy providers who build on top of legacy equipment, some 10+ years old, can’t do. Since Dish doesn’t have a mix of legacy and new base stations, they are able to create the same configuration for all their cell sites. This allows them to test security at a much faster rate than other CSPs due to its simplicity.

Anterix, which offers Private LTE to utilities is able to charge a premium for its spectrum given the ROI for its customers via improved security and automation. The San Diego Electric (SD&E) CEO claims that with Private LTE, they can turn off the power from a down power line before it hits the ground preventing fires from starting. The ROI is enormous since California wildfires resulted in 10B of total damage last year.

From Steel City Capital’s letter, SD&E’s “$50 million payment equates to ~$2.30/MHz Pop, which is a near 40% premium to the $1.68/MHz Pop (weighted average by population) paid for 600 MHz spectrum in the same counties”. If customers are willing to pay top dollar for 4G that is also not cloud-native, it leaves some optimism for what the implied value of Dish’s spectrum is when they rent out slices of their network to enterprises. If Dish’s spectrum is valued at a 40% premium of what they bought it for, their spectrum valuation is 38B, greater than their current 22B equity value.

Since ROI math is tricky for NaaS due to its nascency, let’s use a proven, high ROI use case like Twillio as a base. With their partnership, Dish and AWS are creating APIs for developers “to engage with data on DISH network attributes such as user equipment latency, bit rate, quality of service, and equipment location”. The location data would allow Dish / AWS to pair messaging services with contextual advertising and act as a CPaaS provider. Twillio has seen tremendous success in the space, but it’d be a higher margin for AWS / Dish given that they’d cut out the middle man and Dish offers additional capabilities like location. While Dish itself isn’t a viable CPaaS player given the lack of a developer ecosystem, their integration with AWS APIs allows them to offer a great product that may steal some market share. They’d also be able to offer broader experiences than Twillio, in certain aspects of the customer experience journey. For a B2B2C model, Epic developers could use Dish/AWS APIs to optimize latency for a gamer’s device on a pay-per-play model. Users could pay for this optimized latency service for competitive matchups resulting in improved gamer engagement and an additional revenue stream for Epic. In these cases, Dish is able to combine all of the facets of 5G — AWS APIs, 5G’s ability to slice the network, and improved latency — to create a high ROI for enterprises.

Since 5G has endless optionality, Dish’s planned usage-based model (look at the DigitalRoute vendor Press Release) works for both the company and Dish as it scales up as its 5G use cases do — say they start using 5G for IoT with cameras in stadiums then move to also offer it for play-by-play betting— similar to the AWS model. As a result, Dish directly benefits from more innovation by developers on AWS who can launch go-to-market applications faster than ever before given the cloud-native network. As companies gain advantages with the use of 5G, others will likely follow (this is what we’re seeing in the utility space), so that they’re not at a competitive disadvantage which then leads to more usage of 5G as companies look to find differentiation on 5G use cases. This should result in further TAM expansion and high ARRs.

Compared to non-cloud native providers, Dish should have faster speed to market on new 5G applications. Their AWS partnership allows developers to use continuous integration (CI) and delivery (CD). CI automates the process where combine their application-specific code to the central repository and allows developers to “address bugs quicker, improve software quality, and reduce the time it takes to validate and release new software updates” while CD automates testing like UI/API testing before deployment via the AWS cloud. An AWS whitepaper, argues that “what used to take multiple weeks for truckrolls to deploy a service at CSP can now be orchestrated in minutes using Deployment Pipelines”. Speed to market on the deployment of new applications is critical for 5G given its endless possibilities. Enterprises will prefer a dynamic platform that allows them to test and deploy rapidly, and this improvement in time and agility compounds over time. Dish customers are also able to work with familiar AWS APIs, and Dish is able to attach itself to the entire AWS developer ecosystem like with AWS Panorama Appliance for industrial IoT.

Long-Term Margins

The current state of wireless players includes the Big 3 chipping away for retail customers that have decreasing ARPUs due to the commoditization of data. O-RAN and the enterprise market create 3 new ways that can potentially improve margins. While some of these might work and many might fail, it’s too early to decide what will truly drive value for CSP, however, it is clear that the enterprise business offers a chance to reverse current wireless trends.

First, CSP-specific APIs/Applications. These could include “APIs..[that can] enable an industrial automation application to gain direct access to quality-of-service parameters in the 5G network, or an automated vehicle to trigger the creation of a new user plane instance in a closer location as it moves, or a service assurance application to tap into network analytics.” The API that AWS/Dish has created for latency/location is an example of CSP-specific offerings. Churn should be lower since enterprises will build solutions on specific applications / APIs, so there’s integration apart from SIMs.

Second, firms can bundle high-margin adjacent “as a services” like security, managed services, Communication, Unified Communication, Infrastructure, and WAN Optimization. These create value for enterprises like, billing-as-a service which is important for B2B2X models where enterprises are re-selling network access as a part of their current offering (Epic example above) and need a way to then bill their consumer for that usage. CSPs are the right partner for this since they have a more robust billing system that enterprises can utilize rather than go through a 3rd party. It’s a win-win since enterprises can add new revenue streams with ease and Dish expands its TAM. Dish and Allot are partnering to offer security as a service. In Allot’s surveys, 25%-40% of retail and enterprise consumers, who want an additional security layer that they can manage, would pay a 5-8% fee on top of the network fee. In this partnership, these services could be 70% GM for Dish because they are extremely well-positioned to sell Security-as-a-service (SaaSe) since they are a trusted brand, have a billing relationship with customers, and have frequent interactions with users. Even though Dish doesn’t control the technology, Allot and maybe, DigitalRoute with billing, are willing to share 50-70% of the revenue with the provider because SaaSe adoption is low unless the CSP sells it while it also significantly reduces their S&M since the CSP manages the touchpoints for sales. Services could be a large market as Verizon states that these services are what “create a pretty compelling revenue case” for the enterprise market. The bundles, in addition to CSPs creating an ecosystem of products around each use case, should reduce churn. Dish is attempting this with their Parkifi acquisition and agreement with Relay from Republic Wireless while Verizon has a partnership for Clover payment processors and has created their own, proprietary Critical Asset Sensor.

Third, O-RAN is anticipated to reduce OPEX using end-to-end automation. While experts believe these benefits are years out given the lack of structured data to build ML models, automation in wireless networks is estimated to reduce staff operating costs by ~15%, lower power consumption by 30-55% by “predict[ing] traffic patterns, traffic load, and end-user needs”, and also reduce network downtime by ~35% by pre-empting maintenance. Overall, O-RAN proponents argue it’ll cut OPEX by 30%, and although current networks are somewhat virtualized, there haven’t been significant cost reductions given limited automated processes (only 35% of customer orders are fully automated), With no legacy equipment and virtualization from day one, maintenance capital expenditures should be lower especially considering that Dish is expected to spend less on deployment than Verizon will on maintenance.

While this analysis applies to wireless players in general, Dish is the most pureplay enterprise 5G CSP which gets them the most exposure (as a % of revenue) to services/enterprise margins. Even if O-RAN is adopted by everyone, O-RAN reduces capital needs so that Dish can feasibly enter the market. T-Mobile also that argues brownfield O-RAN adoption potentially will not reap any cost benefits that Dish will gain as a greenfield (although, ATT says otherwise) and CSPs may take longer to enter O-RAN due to integration with legacy systems. This gives Dish a nice head start when getting enterprises onboard, and then keeping them on board with product / API integration. Regardless, improved wireless profitability is not zero-sum given that investors could see a double at current prices if Dish maintains minimal market share but secular trends play out.

Valuation

5G offers optionality in this space, but the existing market is already close to 50B for the Big 3 for government, SMBs, large enterprises, and wholesaling. With 5G, there is the enabling of 1B+ more IoT devices, fixed wireless for rural homes, autonomous driving, B2B2X use cases, adjacent services that can be launched on top, replacement VPNs, and more.

Long term estimates for Dish are low given execution risk, but currently priced in 2025 enterprise revenue sits at roughly 3.8B

On the existing enterprise market, there are currently millions of IoT devices that are connected to 3G and need to make a jump to 5G with the 3G sunset in late ‘22. As they make the jump, Dish has the opportunity to capture some of these customers, in addition to stealing some MVNO wholesaling market. This market itself is 50B as of today.

With IoT, between now and 2025, there will be 2.6B MORE devices in North America by 2020, and assuming that 75% of those are in the US, there will be 1.95B devices that could potentially be powered by 5G. Even if just 10% of these devices are enabled by 5G at Verizon’s lower-end enterprise pricing of $6 per device/per month, that would be a 14B revenue opportunity by 2025.

Sticking with just IoT, Allot suggests 25-40% uptake at a 6-8% fee on top. Given Verizon’s comments on these “as-a-services”, Allot being just one service that could get 25%+ buy-in, and the large number of services that could be bundled, this could be at least 50% of the IoT opportunity. In this case, it would add 7B in potential TAM

Considering that this only includes 3 segments, the TAM is already 71B, so in order to meet current estimates, Dish would only need ~6% of this pie. Given the Walgreens partnership, Dish is likely more competitive than anticipated given their security/speed to market differentiation. As a result, these estimates should likely be raised as deployment targets are met and enterprise contracts are released.

With the characteristics above — large TAM, mission-critical, high ARR, growth opportunities, 60-70% GM range, high switching costs due to deep integration, the ability to sell adjacent services, and decreased maintenance CAPEX with cloud-native economics — Dish would likely rotate closer to something like a cloud multiple. The margin analysis below assumes a middle ground in wireless margins between a fully O-RAN network and Verizon, in addition to a 20% contribution from high margin adjacent services. If some of these things play out, Dish could be generating 20%+ normalized net income margins which are eye to eye with other SaaS / Cloud businesses.

If Dish re-rates to a multiple closer to low-growth cloud multiples, its enterprise business would be equal to 38B in equity value using 2025 sell-side revenue and a 10x revenue multiple. Combined with a ~4% retail wireless market share (sell-side) at a 10% NI margin and 15x earnings multiple, Dish would add an 8B from retail resulting in 46B of total equity value and a 20% 5-year IRR. A lot of this is me hypothesizing given that 5G, in combination with Dish’s deployment is in early stages, however, even with limited puzzle pieces on the board, it seems clear that the market is misjudging Dish’s potential.

Downside Scenarios

In 2019, there was 187B in wireless revenue resulting in a 187B in enterprise value (for PCS, ESMR, AWS, BRS, and 700 MHz license holders) at a 10% net income margin and 10x earnings multiple (function of the durability of moat despite declining earnings). With just this current TAM, Dish would need roughly 12.5% (Sprint had 17%) of the current wireless market to equal its current ~22B equity value (assuming its satellite TV EV = debt). There’s a risk that Dish doesn’t get this share due to the Big 3’s dominance, but Dish has 27B in spectrum assets that they can sell if they aren’t a viable competitor. The downside is that they overspend on the network and sell their spectrum at slight appreciation (sell-side values) after meeting FCC requirements. My analysis suggests a 27% absolute downside case.

However, if Dish achieves something close to such market share, the current equity value would then ignore the paradigm shift that’s occurring in enterprise wireless via 5G like the internet of things, automated cars, etc...

Please, this is not investment advice, and do your own work. I enjoyed covering this company for the last month, so please DM on Twitter (@hcompounders) / email me (rahulbav@wharton.upenn.edu) with any feedback / data inquiries. As a young investor, I’m constantly looking for new ways to learn, so I’d really appreciate any feedback from anyone, especially telecom experts who know this space a lot better than I do. Thanks!

*Additionally, given the catalyst heavy nature of Dish, I’ll try my best to make this a live document that captures future news (deployments, permits, partners, quarters)